Private Cloud is a Fantasy

According to David Linthicum's cloud blog on InfoWorld. http://www.infoworld.com/article/3032308/cloud-computing/wake-up-the-private-cloud-fantasy-is-over.html#tk.rss_cloudcomputing

Linthicum cites a new study that shows the public cloud market is four times larger than the private cloud market. The reality is that public clouds currently supports around 10 - 15% of production workloads. The article is based on an arbitary classification of private cloud that compares apples with oranges.

For some bizarre reason InfoWorld keeps presenting David Linthicum as some sort of credible authority even though his track record for prediction is worse than Gartner. For example who else remembers this clanker from Linthicum in 2013?

http://www.infoworld.com/article/2611432/cloud-computing/windows-azure-users--be-afraid-of-microsoft-s-shake-up.html

"First, it does not appear that the level of innovation will rise at Microsoft, specifically around its PaaS and IaaS offerings. Microsoft has been playing follow the leader -- specifically, Amazon Web Services, which is right down the street from Microsoft's campus -- when Microsoft really should be innovating to be the leader. However, doing so takes creativity, an attribute Microsoft has been lacking. (Look no further than the Surface for proof.)"

Don't you just love the not so subtle dig at Surface as proof of Microsoft's lack of leadership and innovation? Lucky nobody ever reads old blog posts. Zero from two in one short paragraph.

The private cloud fantasy comment is based on a blog post on Wikibon. http://wikibon.com/public-cloud-iaas-is-3-5x-the-size-of-true-private-cloud-adoption/

Citing Wikibon as a credible source of data and analysis is bad enough, but when you actually read the Wikibon article the definition of "true" private cloud is defined is such an unconventional way that it defies all logic and common sense. Under the Wikibon definition HPE and Oracle are larger private cloud vendors than VMware, and NetApp and Cisco are larger than Microsoft! Nutanix is almost as large as Microsoft and RedHat is so small it is lumped in with others!

My company Dell is also lumped in with others, even though we are the only company shipping both Evo Rail and Microsft CPS, and the majority of Nutanix implementations are built on Dell XC appliances. How does HPE come in at number one when the Helion hybrid strategy is in tatters and their PaaS is just rebadged Cloud Foundry? Exactly what technologies are they tracking, or is the data based on POOMA analysis?

This arbitrary definition of "true" private cloud is irrelevant. It seems they have measured the market largely on reported shipped unit of converged infrastructure. Defining private cloud based on converged or hyper converged platforms is a joke, in most cases converged infrastructure is more about marketing and packaging than it is around "cloud" capability.

Customers deploy infrastructure that meets their specific needs, not some arbitrary definitions of functionality that private cloud is supposed to fit into. This definition excludes pretty much all virtualisation infrastructure and all implementations that are relatively static and do not justify the effort and expense of deploying and maintaining orchestrations solutions.

Under this narrow definition I am surprised that the "true"" private cloud market is so large.

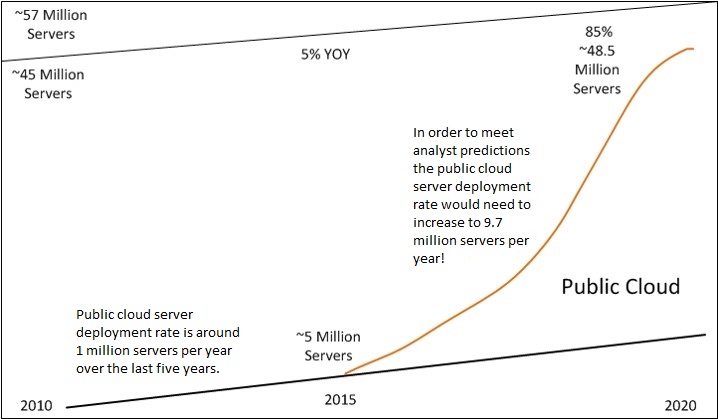

A much better way to assess public cloud adoption is to look at total number of servers shipped and to determine how many servers go to public cloud vendors. My estimate based on some work I did last year is that all public cloud providers combined have around 5 million servers of deployed capacity out of the roughly 45 million servers in production today, or about 10 - 15% of global server compute. Server shipments are growing at a low but steady rate of around 5% per year. Given that the average life of a server is five years this means that in order to achieve 85% market share by 2020 public cloud vendors would need to deploy approximately 9.7 million servers per year. That would be double the entire deployed capacity every year.

Clearly this sort of sustained growth rate is impossible, the numbers are too huge to contemplate, and the capital investment required is beyond any cloud vendor. It is easy to get excited with the growth rates in the early years of cloud, but it is extremely misleading to look at extrapolations from a zero base and make future projections based on them. The most likely scenario is that cloud vendors will continue to deploy at current rate, which will take a decade or more to build the scale of infrastructure required to support the majority of global compute workloads.

What I really object to with Linthicum is not the lack of rigour or the cherry picking of dodgy analyst blogs or the chasing of shiny new toys like a cat with a laser pointer, it is the pure propaganda of trying to make organisations and technologists feel like they are stupid if they are not pushing everything to public cloud right now.

Every organisation is different, every workload and requirement needs to be treated as unique when starting down the cloud path. For some organisations it is perfectly reasonable to go all in with cloud, however for many it is not. There is no rush, it is not going away, and services are getting better all the time. When organisations start moving workloads that make sense pretty soon they begin to realise the strengths and weaknesses of public cloud versus private cloud versus legacy virtualisation platforms.